Climate impact

Finland and Sweden have some of the world’s highest shares of bioenergy in pulp and paper industry. This is one of the main reasons why the industry in Finland has had a carbon intensity of 14 tCO2/TJ and Sweden just 4 tCO2/TJ, compared with the global average of 35 tCO2/TJ. The low carbon intensities have saved 0.7 MtCO2 in Finland and 2.1 MtCO2 in Sweden per year relative to the OECD average.

For countries both inside and outside of OECD, we have considered reaching Finland’s annual reduction rate in carbon intensity. Additionally, for OECD countries we have looked at achieving Finland’s average absolute carbon intensity.

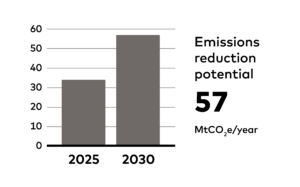

The more moderate approach would reduce emissions by 20% below OECD average, whereas the more ambitious one would result in cutting emissions by 30%. The total emission reduction potential would be 57 Mt in 2030.

Success factors

The pulp and paper industry in Nordic industries has achieved a low carbon intensity expressed in CO2 emissions per energy used. Typically the levels have been less than two-thirds of the OECD average and one-third to one-half of the world average.

The pulp and paper industry derives a high share of energy from biomass by using waste and residues from their main raw material, wood. Over the period 2003–13, the industry in Finland and Sweden got 76% and 89% of its non-electricity final energy consumption from bioenergy, respectively. By comparison, the OECD average for 2013 was only 54% and the global average 39%.

The industry started to move away from oil after the oil crises. Factories also reduced pollution by burning residues rather than releasing them into nearby waterways. In Sweden green certificates reward electricity from renewables, making it profitable to invest in electricity generation based on by-products such as black liquor and forestry residues.

“Increased bioenergy use relies on the availability of sustainable biomass resources.”

Costs

The costs can vary greatly depending on local circumstances. We have derived a cost estimate from replacing coal with biomass in the chemical industry with both new build and retrofits as the closest analogue. In reality, the costs may be a good deal smaller since more of the biomass used in the pulp and paper industry will come from industry byproducts and waste.

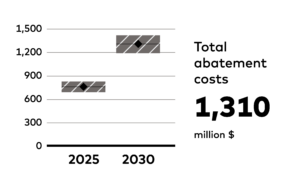

The abatement cost has been estimated at 23 $/ tCO2, leading to a total cost of $1,310 million in 2030.

Co-benefits

Producing bioenergy in industry can provide some co-benefits, including

- reducing fuel imports

- improving energy security

- creating local jobs

Barriers and drivers

The most important enabler for this solution is the availability of sufficient biomass resources from wood waste and by-products. Biomass supply from wood wastes may be considerably lower in countries which do not have a large forestry industry of their own and which need to import pulp. The carbon intensity can be reduced by supplying biomass from other sources as well, but this would both increase costs and raise more questions about sustainability. For a discussion on the availability of sustainable biomass, see section Is biomass use sustainable? in the report.

High recycling rates could paradoxically make high biomass use more challenging by reducing the amount of wood wastes available per unit of produced paper. However, the net effect is not clear, since the use of recycled paper also reduces the total energy demand.

RELATED SOLUTIONS